Prime Minister Gaston Browne is asking Parliament to approve:

• EC$405 million in borrowing to finance 2026 operations, and

• EC$1.2 billion more for “liability management,” refinancing, and other obligations.

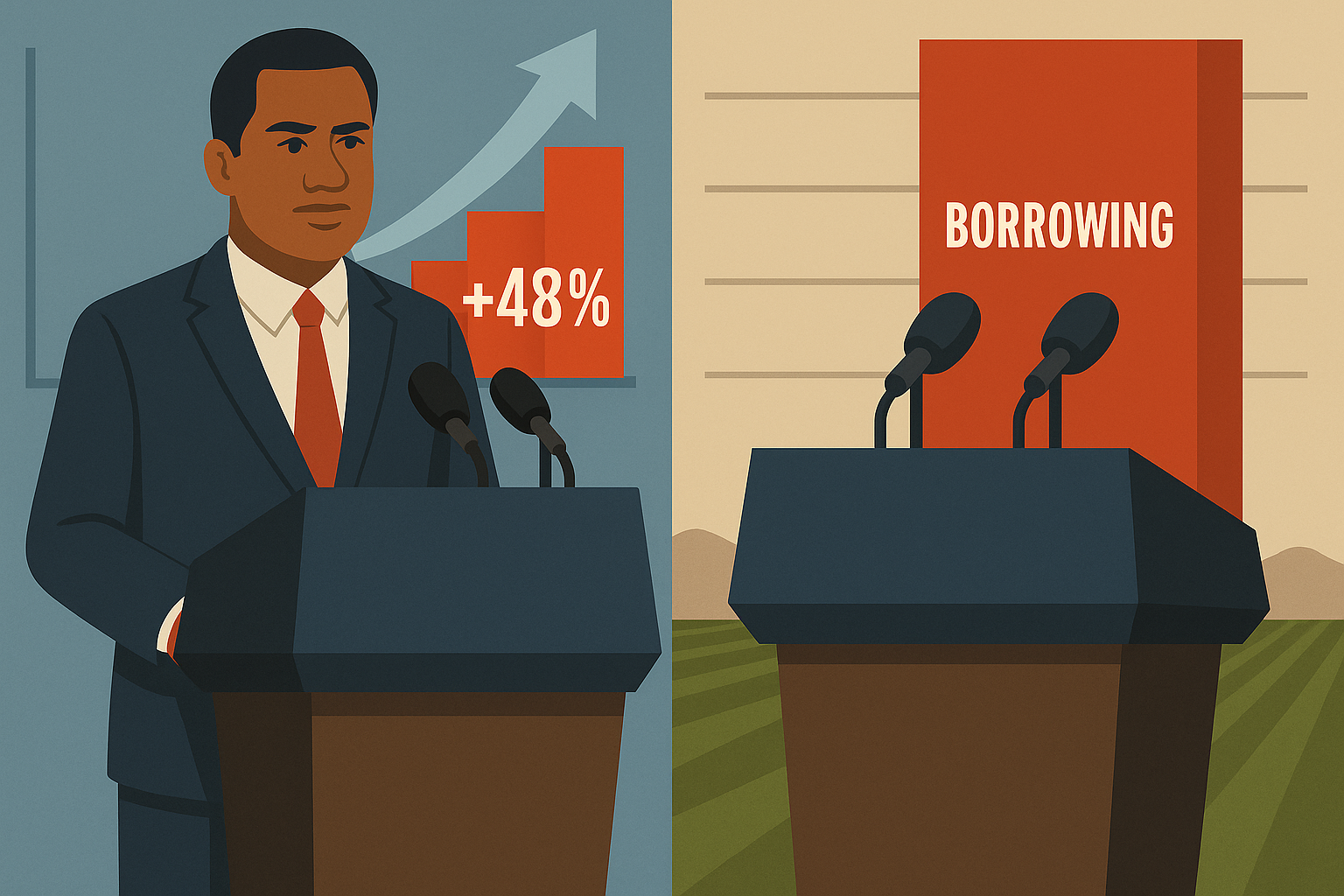

That is EC$1.6 billion in new borrowing authority in a year allegedly built on record-breaking tourism growth.

This raises urgent questions:

If visitor spending is truly expanding the revenue base, why must the country rely on unprecedented levels of borrowing just to keep the government functioning?

Why do record tourism numbers not translate into reduced debt and improved fiscal stability — as they logically should?

Something does not add up.

if the revenue story were real, fiscal dependence on borrowing should be declining, not expanding.

Additionally, The Prime Minister described tourism as “one of the most resilient revenue streams” yet independent assessments — including from the IMF, the World Bank, and the WTTC — consistently warn that Antigua & Barbuda remains:

• highly vulnerable to external shocks,

• overdependent on tourism,

• exposed to climate and economic risks, and

• carrying a debt burden that requires discipline, not exuberance.

If tourism were as resilient as claimed, external institutions would signal reduced vulnerability. Instead, they stress fragility — the exact opposite of the political narrative.

If tourism is so resilient, why does every credible external report still describe Antigua & Barbuda as among the most economically vulnerable states in the region? If visitor spending is at record highs, why hasn’t the country’s vulnerability decreased in any meaningful way?

Again: the math is not “mathing”.

When were the Ministries of Tourism, Aviation, Finance, the Tourism Authority, the Port Authority, the Airport Authority, and all related state entities last audited by the Director of Audit?

Under Sections 88–92 of the Constitution, the Director of Audit must:

• Audit every ministry, department, and public body annually.

• Submit audited accounts to Parliament.

• Publish findings for public accountability.

These audits are not optional. They are constitutional safeguards.

Yet for years, the public has heard almost nothing about:

• Tourism Authority audits

• Port Authority audits

• Cruise and airlift revenue audits

• Accommodation tax audits

• Guest levy audits

• Heritage site audits

• Hotel and Airbnb compliance audits

• CIP tourism-linked revenue audits.

Without those audits, the Government’s tourism figures — whether expressed as $2.4 billion, EC$2.4 billion, or a 48% increase — are unaudited assertions, not verified financial data.

The truth is, the Prime Minister cannot claim record-breaking tourism performance when the nation has not seen audited accounts for the very agencies responsible for collecting, reporting, and managing tourism revenue. Until audited reports are laid before Parliament, every claim is unsubstantiated.

The Prime Minister may celebrate a 48% rise in visitor spending, but without:

• verified audited accounts,

• transparent data sources,

• reconciliation with international economic assessments, and

• fiscal outcomes that match the rhetoric, the public has no reason to accept these numbers as credible.

The Constitution requires annual, independent audits precisely to prevent governments from presenting unaudited numbers as fact. Until those audits are published, the tourism narrative remains politically convenient, economically inconsistent, and constitutionally unsupported.

Yes, the numbers may be impressive — but without audits, they are not trustworthy. The math is simply not “mathing”.